AMINA Bank AG

AMINA Bank AG

AMINA UK

AMINA UK

AMINA Hong Kong

AMINA Hong Kong

AMINA EU

AMINA EU

In early 2026, markets delivered the first genuine stress test of tokenised financial infrastructure. Sovereign bond volatility rippled through the crypto market. Central bank transitions rattled market sentiment. Yet $24.7 billion sitting in on chain real-world assets didn’t unwind. Trading continued and settlement remained instantaneous. BlackRock’s BUIDL fund listed on Uniswap – its first DeFi integration – without operational issues.

That resilience is the real story: the fact that the infrastructure works under pressure. More than two-fifths of this market sits in U.S. Treasuries, up from under $1 billion in early 2024. Tokenised commodities have grown 260% year-over-year. Private credit also expanded at 185% per quarter.

Three numbers explain what has changed, and why the next phase of growth will look fundamentally different from the last.

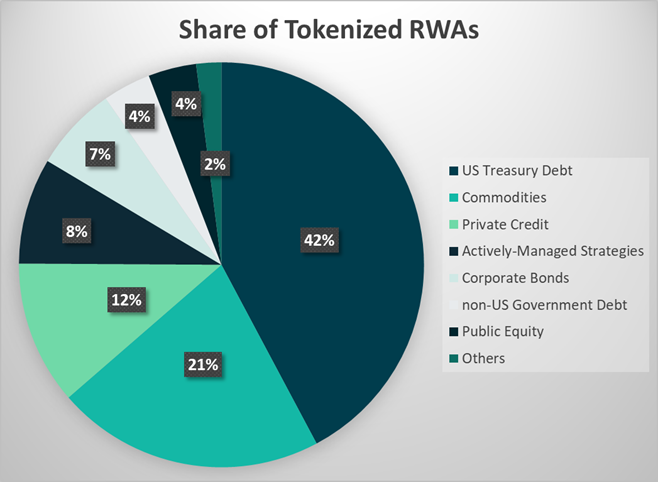

Number One: 42%

The concentration of the entire tokenised RWA market currently held in U.S. Treasury debt.

Figure 1: US Treasury Debt Instruments Dominate Tokenised Assets

Source: RWA.xyz (As on 12.02.2026)

More than two-fifths of all onchain real-world assets – $10.38 billion – sit in the boring, safest, most institutional instrument on earth. BlackRock’s BUIDL fund holds $2.17 billion, but it is no longer the largest tokenised Treasury product. Circle’s USYC overtook it in late January 2026 but currently sits at $1.56 billion, having grown 11% in the past 30 days while BUIDL contracted 2.85%. Ondo’s Dollar Yield Fund holds $1.3 billion. Franklin Templeton’s Onchain US Government Money Fund ($800 million) integrated directly as exchange collateral.

The difference between the winners and laggards is not brand recognition – it is distribution architecture. Circle’s USYC grew 11% in the past 30 days while BUIDL contracted 2.85%. USYC embedded itself into Binance’s collateral rails four months before BUIDL, capturing the flow of institutional derivatives margin. As JPMorgan framed it: tokenised Treasuries are not an alternative to stablecoins but an evolution of them – programmable cash equivalents that settle faster and integrate into collateral systems with less operational overhead.

Regulatory infrastructure is catching up to match. The International Organization of Securities Commissions (IOSCO) now explicitly recognizes tokenised money market funds as reserve assets for stablecoins and collateral for crypto transactions.

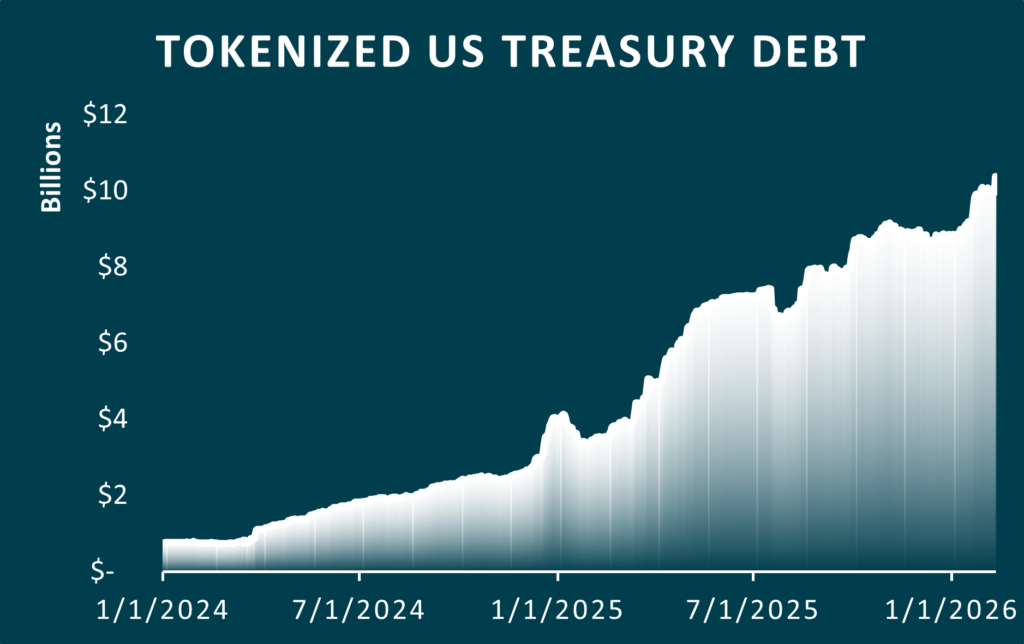

Figure 2: Tokenised US Treasury Debt Instruments Surpass $10 billion

Source: RWA.xyz (As on 12.01.2026)

The yield is a modest 3.5% to 5% APY, and that is precisely the point. In a market where stablecoins yield near zero, tokenised Treasuries offer risk-free returns without exiting crypto rails. For corporate treasuries managing billions in working capital, that efficiency is not marginal. It is structural.

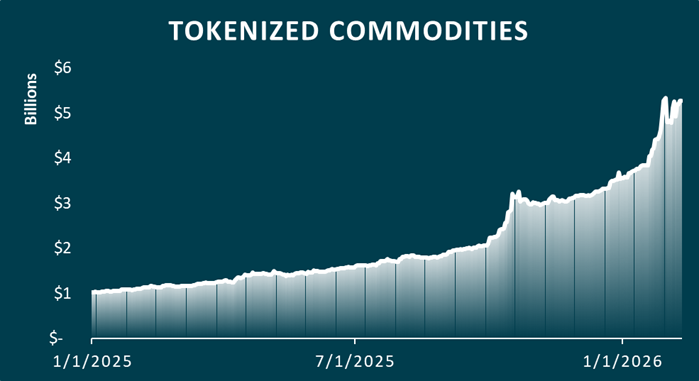

Number Two: 360%

The year-on-year growth of tokenised commodities.

This is the fastest growing vertical in the entire RWA market. But the growth rate is an artefact of starting from a small base. What matters more is the dynamic driving it: investors are treating tokenised gold as “Safe Haven 2.0.” Bitcoin has traded like a risk asset, down 10% over the past year. Gold has functioned as an uncorrelated store of value. Tokenisation adds velocity to that stability — fractional ownership down to $0.01, instant settlement at 3:00 AM on a Sunday, direct redemption for physical bars at 430 tokens.

Tokenised commodities crossed $6.1 billion this week, adding $2 billion since January 1 alone. Gold trades at $5,080 per ounce, up 13% in January and 75% over the past year. But the on-chain version is moving faster than physical metal.

Figure 3: Growth in Tokenised Commodities Moves In Tandem To The Underlying

Source: RWA.xyz (As on 12.02.2026)

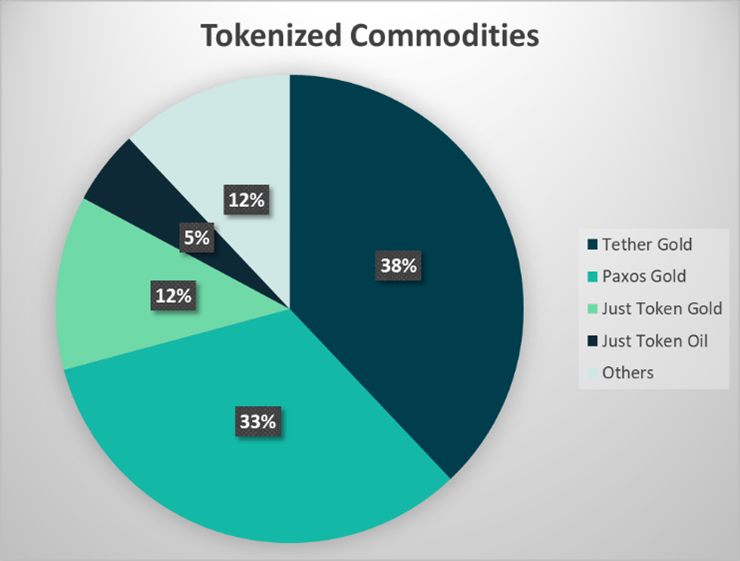

Tether Gold (XAUt) now holds $2.7 billion in market cap, up 51.6% in the past month. Paxos Gold (PAXG) sits at $2.3 billion, up 133.2%, with $248 million in fresh inflows in January alone. Tether has accumulated an estimated 140 metric tons of physical bullion—turning the world’s largest stablecoin issuer into a sovereign-scale force in precious metals. Together, these two products represent 83% of the entire tokenised commodities market, backed by audited physical reserves, trading continuously across global exchanges. James Harris, CEO of Tesseract Group, captured the shift: “The growing traction of tokenised gold has improved gold’s utility, particularly around transferability and divisibility, while bitcoin continues to trade more like a risk asset in periods of macro uncertainty.”

The $6.1 billion figure represents gold’s dominance at 73% of all tokenised commodities. The concentration, and its implications, is notable. If tokenisation can add velocity and accessibility to the world’s oldest safe haven asset, the model extends well beyond precious metals.

Figure 4: Gold Dominates Tokenised Commodities at 73%

Source: RWA.xyz

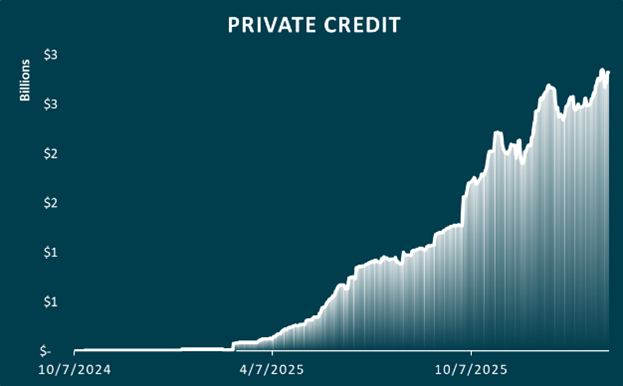

Number Three: 185%

The quarterly growth rate of tokenised Private Credit. (Not annual. Quarterly.)

The growth is particularly notable because Private Credit was assumed to be resistant to tokenisation. These are bespoke, illiquid, relationship-driven instruments, the type of assets that traditionally live in spreadsheets, and legal documentation. Although this category barely registered two years ago. Today it stands at $2.8 billion and is expanding faster than any other RWA segment — growing at 185% per quarter while Corporate Bonds, supposedly the “easier” fixed-income opportunity, lag at $1.7 billion.

If Treasuries represent the foundation of institutional tokenisation, Private Credit is emerging as its most dynamic vertical.

Figure 5: Tokenised Private Credit Grows By 1248% in 1-Year

Source: RWA.xyz (As on 12.02.2026)

The mechanism is collateral mobility. Tokenisation is not merely digitising Private Credit but is converting locked capital into programmable instruments that can move across platforms. The same principle applies across asset classes. Ondo Finance demonstrated this operational reality by tokenising BitGo stock within 15 minutes of its trading debut. They are now running 200+ tokenised stocks and ETFs, scaling toward thousands.

Min Lin, Ondo’s managing director of global expansion, frames this as a deliberate design choice: “The wrapper model has been widely adopted. Stablecoins are essentially wrapped U.S. dollars and we have adopted a very similar model.”

The implication is clear. If stocks can be wrapped in 15 minutes and Private Credit can grow at 185% quarterly, the $127 trillion global equities market and $1.5 trillion Private Credit market are no longer theoretical targets. They are addressable markets with established technical pathways.

The Structural Divergence

Divergence is what matters. Tokenisation has reached a point where price action and structural progress no longer move in lockstep. Early 2026 delivered the first genuine stress test of this infrastructure. Market volatility exposed crypto’s sensitivity to sovereign bond markets and central bank transitions. Yet trading in tokenised RWAs continued. Settlement remained instantaneous. The infrastructure did not break down. In fact, it matured through stress.

The three numbers above — 42% concentration in Treasuries, 360% growth in commodities, 185% growth in private credit — describe a market that has crossed from experimental to operational. Treasuries as collateral infrastructure, commodities as velocity-enhanced safe havens, private credit as the asset class that proved the model by defying assumptions about what could be tokenised.

The denominator remains vast. Global wealth exceeds $200 trillion. Tokenised RWAs represent 0.012% of that total. But the growth vectors are clear, and the infrastructure to capture them is now in existence.

Disclaimer – Research and Educational Content (Hong Kong)

This document has been prepared by AMINA (Hong Kong) Limited (“AMINA HK”). AMINA HK is a Type 1 (Dealing in Securities), Type 4 (Advising in Securities) and Type 9 (Asset Management) licensed corporation regulated by the Securities and Futures Commission (“SFC”).

WARNING: This document and its contents have not been reviewed by the SFC or any other regulatory authority in Hong Kong. You are advised to exercise caution in relation to the information provided. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document is published solely for informational and educational purposes; it does not constitute an advertisement, a personal recommendation, nor a solicitation or an offer to buy or sell any financial investment, virtual asset or to participate in any particular investment strategy. This document is for publication only on the AMINA HK website, blog, and AMINA HK social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA HK to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA HK. This document is based on various sources, incl. AMINA HK’s internal data. In preparing this document, AMINA HK may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA HK. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, virtual assets, markets or developments. AMINA HK does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA HK’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA HK’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA HK or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances. Investments involve risks, including the possible loss of the principal amount invested. Virtual assets and tokenized assets are highlight volatile, subject to complex regulatory environments, and carry significant market, liquidity and cybersecurity risks. Investors should exercise prudence and their own independent judgment in making their investment decisions. Financial investments and virtual asset services described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA HK and its employees may differ from or be contrary to the opinions expressed in AMINA HK research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA HK. Unless otherwise agreed in writing, AMINA HK expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA HK accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA (Hong Kong) Limited, 15/F Club Lusitano, 16 Ice House Street, Central, Hong Kong