AMINA Bank AG

AMINA Bank AG

AMINA UK

AMINA UK

AMINA Hong Kong

AMINA Hong Kong

AMINA EU

AMINA EU

Introduction

Institutional participation in staking reached a watershed moment in early 2026. Over $58 billion in capital now flows through liquid staking protocols, whilst an additional $19 billion has moved into restaking, according to DeFi Llama. In Europe, several ETPs have launched that stake underlying Ethereum holdings to generate 3–4% yields for fund holders through familiar regulated structures. Custodial banks and institutional-grade service providers are exploring or entering the market, signalling that staking has evolved from a crypto-native activity to a mainstream yield strategy.

For investors and portfolio managers, staking offers a relatively predictable source of yield on long-term holdings of PoS assets.

In this edition of The Bridge, we examine liquid staking and restaking, assess the current state of these markets, and outline recent developments and their implications for institutional participants.

How Institutions Participate: From LST Holdings to Structured vehicles

Staking has rapidly progressed from a retail and crypto-native activity to a mainstream strategy for institutional investors holding crypto assets. In 2025, we saw major institutions from hedge funds to asset managers and even banks actively engaging in staking as a source of yield on long-term holdings. This participation takes several structured forms.

Participation via Liquid Staking Tokens

Many institutional investors participate in staking via holding liquid staking tokens like stETH, rETH or others on their balance sheet. Some fund managers view LSTs as yield-bearing assets analogous to bonds. In some cases, institutions use wrapped staking through DeFi (for example, depositing ETH into Lido directly through custom smart contracts). This approach simplifies operational burden but introduces smart-contract risk and reliance on the LST issuer.

To mitigate custody concerns, a few specialized wrappers have emerged: e.g., Indexed staking funds that hold a basket of LSTs, or tranche products that separate principal and yield (so an institution can choose a fixed-rate tranche). Additionally, some CeFi firms offer tokenized staking products that represent a share in a staking pool (Coinbase’s cbETH is one such token). These effectively give institutions a wrapped position that can be custodied like any other token and is often easier to report and transfer than a native staked position.

Staking via Funds and Structured Vehicles

An emerging route is through staking-oriented funds or ETFs. In Europe, several ETPs now exist that not only hold crypto but also stake it to generate yield for the fund. For example, a Swiss issuer might have an Ethereum ETP that stakes the underlying ETH and periodically distributes the staking rewards to fund holders. This gives traditional investors exposure to staking yields through a familiar instrument. The U.S. is moving in this direction as well. This adds a 3–4% yield on top of price appreciation, which is a compelling proposition for investment committees. Separately, private funds (like venture funds or dedicated staking yield funds) allocate capital to run validators and pass the yield to limited partners. These vehicles often engage in more complex strategies (like using leverage or restaking to boost yields), effectively functioning like fixed income hedge funds in the crypto space.

In summary, institutional participation in staking is maturing from holding liquid staking tokens to potentially directly influencing staking ecosystems (through governance of LST DAOs or running validators). But one theme is common: abstraction and integration. Staking is being abstracted into familiar investment formats and integrated into institutional-grade custody and reporting systems.

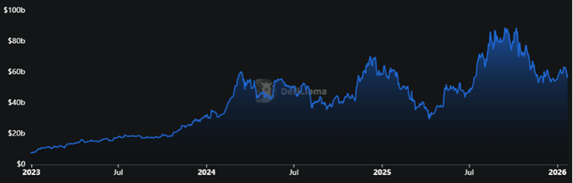

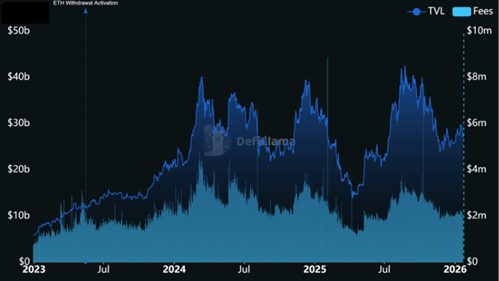

The $77 Billion Staking Market: Liquid Staking and Restaking

At the time of writing, over $58.33 billion in DeFi TVL is in liquid staking, with an additional $19.63 billion in restaking protocols. This represents a market that has grown substantially post-Merge and demonstrates institutional demand for yield-bearing infrastructure participation.

Figure 1: Total value locked in liquid staking protocols has exceeded $58.33 billion

Source: DeFi Llama (27 January 2026)

Figure 2: Restaking TVL across DeFi currently stands at $19.63 billion

Source: DeFi Llama (27 January 2026)

Liquid Staking: Solving the Capital Lock-Up Problem

Leading liquid staking protocols for Ethereum have grown substantially post-Merge, now securing a significant share of ETH’s supply. The sector’s top protocol is Lido with a TVL of over $27.6 billion. This shows Lido’s dominance at over 47.41% of all staked ETH TVL. Its stETH token enjoys deep liquidity and DeFi integration, contributing to a strong network effect (users prefer the LST with the most utility, which further entrenches Lido’s lead).

Figure 3: Lido has a TVL dominance of over 47% in the ETH liquid staking sector

Source: DeFi Llama (27 January 2026)

Other alternatives have grown as well, emphasizing permissionless node participation and greater geographic/client diversity. For example, Rocket Pool’s rETH is backed by thousands of independent operators worldwide, each required to post a sizable bond in ETH and RPL (Rocket Pool’s token) to align incentives. This design offers increased slashing protection, as any validator losses are first covered by the operator’s bonded stake. Centralized exchanges like Coinbase also constitute a large share of staked ETH through custodial offerings and an LST (cbETH).

Restaking: Capital Efficiency Through Layered Security

With over $19.63 billion in restaked TVL, it is abundantly clear that there is a huge demand for additional yield on top of native staking.

EigenCloud (formerly called EigenLayer) on Ethereum is the pioneering restaking protocol. At a high level, EigenCloud creates a marketplace between restakers (ETH stakers seeking higher rewards) and AVSs (off-chain or cross-chain services that need decentralised security). When a user restakes via EigenCloud, they either directly use their validator (if they are a solo staker) or delegate their staked ETH/LST to a third-party operator who will run the required software for various AVSs. EigenCloud works by placing the staked asset (or liquid staking token) under additional rules. By opting in, the restaker accepts that their stake can now be penalised not only for Ethereum-level misconduct, but also if the operator fails to perform correctly for any of the services they choose to secure. In other words, poor behaviour in one attached service can result in a loss on the original stake. In return for taking on this extra risk, restakers earn additional rewards, paid either in ETH or in the service’s own token, depending on how that service is structured.

Key entities in restaking:

- Restaker: An ETH holder, for example, who has staked (natively or via an LST) and opts into restaking. The restaker is essentially staking again on new services, and bears the risk of additional slashing. They either run a validator themselves for each AVS or appoint an Operator.

- Operator: A validator (could be the restaker or a third party) who actually runs the nodes/software for the AVS. Operators interface with each AVS (running oracle nodes, bridge validators, etc.) and earn a portion of AVS rewards for their work. In EigenCloud, restakers can delegate to professional operators, similar to how one might delegate tokens to a validator in other networks.

- AVS (Actively Validated Service): Any application or protocol that outsources its security to restaked ETH. Examples include oracle networks, cross-chain bridges, data availability layers, mempool services or even new blockchains that don’t launch their own token. An AVS sets specific rules that if an operator fails or cheats, a slashing event on EigenCloud will be triggered. The AVS usually pays fees or incentives to attract restakers.

- Application (App): The end-user application or ecosystem that the AVS serves. For instance, an AVS can be a price oracle and the App could be a DeFi platform consuming those price feeds.

EigenCloud’s design allows one validator to secure multiple services simultaneously with the same stake, creating pooled security. In principle, if a restaker trusts the risk/return of many AVSs, the same ETH could be reused to validate an oracle network, a bridge and a data layer. This multiplies potential yield.

This greatly lowers the barrier to bootstrapping security for new projects. Rather than convincing thousands of people to stake a new token, a project can tap into Ethereum’s enormous existing validator base by offering a fee to restakers.

Understanding the Mechanisms: LSTs and Restaking Explained

How Liquid Staking Tokens Work

Staking secures a network, but it comes with a trade-off. Capital gets locked up and sidelined from the rest of DeFi. Liquid staking emerged to solve this exact problem. It allows token holders to earn staking rewards while keeping their capital liquid and usable across decentralised markets.

The mechanism is straightforward. A user stakes the network’s native token through a liquid staking protocol and receives a transferable derivative token in return, commonly referred to as a Liquid Staking Derivative (LSD). This derivative represents the underlying staked position and can be deployed across DeFi for lending, trading, or yield strategies, while the original stake continues to contribute to the network’s economic security.

Lido’s stETH on Ethereum is an example. Lido Finance pools user deposits into its validator lots and delegates operations to a roster of professional node operators vetted by Lido’s DAO. In return, Lido issues stETH (the LSD) which is a tokenized claim on the deposited ETH plus any staking rewards. stETH is a rebasing token: its quantity in holder wallets increases daily as rewards accrue, reflecting earned yield. Importantly, stETH remains liquid and can be traded or used as collateral across many platforms, addressing a major pain point for institutions that require flexibility. Lido’s approach abstracts away validator operation while preserving onchain liquidity.

How Restaking Creates Additional Yield

While liquid staking addresses liquidity of staked assets, restaking addresses the capital efficiency and extensibility of staked security. Restaking allows the same staked asset (e.g. ETH) to be used to secure additional protocols or services beyond the original blockchain. Put simply, a user can deposit their LST into a restaking platform, which then leverages that stake to validate new actively validated services (AVS) in exchange for extra yield. It’s analogous to rehypothecation in traditional finance, except the original staker retains ownership and extends their trust to new applications.

EigenCloud on Ethereum is the pioneering restaking protocol. At a high level, EigenCloud creates a marketplace between restakers (ETH stakers seeking higher rewards) and AVSs (off-chain or cross-chain services that need decentralised security). When a user restakes via EigenCloud, they either directly use their validator (if they are a solo staker) or delegate their staked ETH/LST to a third-party operator who will run the required software for various AVSs.

Figure 4: TVL in EigenCloud ETH restaking currently stands at $13.19 billion – close to 96% ETH restaking TVL dominance.

Source: DeFi Llama (27 January 2026)

EigenCloud works by placing the staked asset (or liquid staking token) under additional rules. By opting in, the restaker accepts that their stake can now be penalised not only for Ethereum-level misconduct, but also if the operator fails to perform correctly for any of the services they choose to secure. In other words, poor behaviour in one attached service can result in a loss on the original stake. In return for taking on this extra risk, restakers earn additional rewards, paid either in ETH or in the service’s own token, depending on how that service is structured.

Similar to LSTs which represent a claim on staked positions, liquid restaked tokens (LRTs) are derivative tokens that represent a claim on restaked positions. These allow secondary trading of restaked positions (with the embedded risk/return profile). In 2026 we may even see structured products that tranche restaking yields (e.g. offering a fixed yield to one party and leveraged exposure to another via protocols like Pendle).

Risks Management Framework for Institutional Staking

For institutions, both liquid staking and restaking open new avenues for yield, but also a need for rigorous risk management.

Validator concentration and counterparty risk

In traditional staking, delegating to a single provider or pool concentrates risk. That provider could suffer downtime, slashing, insolvency, or regulatory pressure. The Lido example illustrates this at the network level but the same logic applies at the portfolio level if an institution fails to diversify operators. Best practice is to spread stake across independent validators or use structurally decentralized pools.

In restaking, this risk is amplified. Institutions typically delegate to an operator who may secure multiple services simultaneously. If that operator fails or behaves maliciously, losses can propagate across base staking and all attached AVSs at once—a correlated slashing scenario. This makes operator due diligence critical and argues for distributing restaked exposure across multiple operators rather than concentrating it.

Technical slashing and Lego risk

On Ethereum, slashing is rare and usually tied to clear misconduct such as double-signing. For high-quality operators, the probability of this happening is low and largely operational in nature. The larger risks tend to be key mismanagement or temporary downtime, which are mitigated through mature infrastructure and monitoring.

Meanwhile, restaking introduces Lego risk, which arises from stacking multiple services on the same underlying stake compounds failure probability. Each additional AVS is another block in the stack. If any one fails (due to buggy slashing or faulty oracle data), the entire stake is exposed. Restaking also introduces additional smart-contract risk at the protocol layer. Institutions therefore generally tend to limit AVS exposure to a small, well-understood set rather than maximizing yield through breadth.

Financial and market risk

Staking yields depend on protocol design and network activity. As participation and fees rises, per-validator yield falls. And as MEV rises, yield too rises. Illiquid staking methods introduce exit risk, which liquid staking tokens partially mitigate.

Restaking adds market risk when rewards are paid in AVS tokens. High yields can be offset by token volatility or illiquidity. Even when rewards are paid in ETH, they depend on AVS adoption and usage. Restaked assets may also be sometimes slower to exit, remaining exposed to market risks during cooldown periods. From a portfolio perspective, restaking resembles credit exposure wherein institutions are effectively underwriting protocol failure risk in exchange for a premium.

Composability and inter-protocol risk

Using staking derivatives in DeFi compounds dependencies. An institution staking via Lido and lending stETH inherits exposure to both protocols. Restaking is inherently compositional and additional yield strategies further increase complexity. Each added layer introduces new smart-contract, oracle, and governance risks. Most institutions respond conservatively, preferring simpler structures with fewer moving parts even at the cost of lower yield.

Regulatory and legal risk

Legal treatment of staking remains unsettled. In the EU, MiCA does not regulate staking directly but treats staking-as-a-service as a custody activity, potentially making custodians liable for losses, including slashing. This has material implications for contractual risk allocation.

Restaking is even more ambiguous. It is unclear whether restaking platforms are regulated services or neutral software layers. In the event of losses from AVS failures, institutions may have limited legal recourse. This uncertainty explains why many institutions cap restaking exposure or restrict it to jurisdictions and structures they are comfortable defending legally.

For institutions, staking is increasingly viewed as low-risk, infrastructure-level yield when executed with reputable partners and proper controls. However, restaking sits firmly in a higher-risk, higher-return category. As restaking matures, we expect a convergence of DeFi risk management practices and staking (e.g., insurance products for slashing events, credit-style ratings for AVSs, and potentially regulatory scrutiny (if these arrangements are deemed financial contracts). Over time, as platforms mature and regulatory clarity improves, institutional confidence may grow but for now, restraint remains.

Conclusion

In summary, institutional staking structures are converging towards solutions that mimic traditional financial services: assets stay with qualified custodians, risk is mitigated via contracts and insurance, liquidity is managed via tradable wrappers, and everything is packaged in investment-friendly vehicles when needed. The direction is clear: make staking as easy as buying a money market fund, and as acceptable from a regulatory perspective as holding any other yielding asset.

As this happens, staking will move from a peripheral activity to a core allocation in institutional portfolios holding crypto. The fact that even custodial banks and big financial names are exploring or entering the staking business (through partnerships or tech integration) underscores that staking is becoming an extension of the conventional financial system in many respects – albeit one that still demands understanding of unique crypto risks.

—

Disclaimer – Research and Educational Content (Hong Kong)

This document has been prepared by AMINA (Hong Kong) Limited (“AMINA HK”). AMINA HK is a Type 1 (Dealing in Securities), Type 4 (Advising in Securities) and Type 9 (Asset Management) licensed corporation regulated by the Securities and Futures Commission (“SFC”).

WARNING: This document and its contents have not been reviewed by the SFC or any other regulatory authority in Hong Kong. You are advised to exercise caution in relation to the information provided. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document is published solely for informational and educational purposes; it does not constitute an advertisement, a personal recommendation, nor a solicitation or an offer to buy or sell any financial investment, virtual asset or to participate in any particular investment strategy. This document is for publication only on the AMINA HK website, blog, and AMINA HK social media accounts as permitted by applicable law. It is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or would subject AMINA HK to any registration or licensing requirement within such jurisdiction.

Research will initiate, update and cease coverage solely at the discretion of AMINA HK. This document is based on various sources, incl. AMINA HK’s internal data. In preparing this document, AMINA HK may have made limited use of artificial intelligence–enabled tools to assist with research, summarisation, and drafting, with all content subject to human review and validation.

No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained in this document, except with respect to information concerning AMINA HK. The information is not intended to be a complete statement or summary of the subjects alluded to in the document, whereas general information, financial investments, virtual assets, markets or developments. AMINA HK does not undertake to update or keep current information. Any statements contained in this document attributed to a third party represent AMINA HK’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party.

Any formulas, equations, or prices stated in this document are for informational or explanatory purposes only and do not represent valuations for individual investments. There is no representation that any transaction can or could have been affected at those formulas, equations, or prices, and any formula(s), equation(s), or price(s) do not necessarily reflect AMINA HK’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different assumptions by AMINA HK or any other source may yield substantially different results.

Nothing in this document constitutes a representation that any investment strategy or investment is suitable or appropriate to an investor’s individual circumstances. Investments involve risks, including the possible loss of the principal amount invested. Virtual assets and tokenized assets are highlight volatile, subject to complex regulatory environments, and carry significant market, liquidity and cybersecurity risks. Investors should exercise prudence and their own independent judgment in making their investment decisions. Financial investments and virtual asset services described in the document may not be eligible for sale in all jurisdictions or to certain categories of investors. Certain services and products are subject to legal restrictions and cannot be offered on an unrestricted basis to certain investors. Recipients are therefore asked to consult the restrictions relating to investments, products or services for further information. Furthermore, recipients may consult their legal/tax advisors should they require any clarifications.

At any time, investment decisions (including, among others, deposit, buy, sell or hold investments) made by AMINA HK and its employees may differ from or be contrary to the opinions expressed in AMINA HK research publications.

This document may not be reproduced, or copies circulated without prior authority of AMINA HK. Unless otherwise agreed in writing, AMINA HK expressly prohibits the distribution and transfer of this document to third parties for any reason. AMINA HK accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distribution of this document.

©2026 AMINA (Hong Kong) Limited, 15/F Club Lusitano, 16 Ice House Street, Central, Hong Kong